Morning Note: Market News and an Update from Personal Assets Trust.

Market News

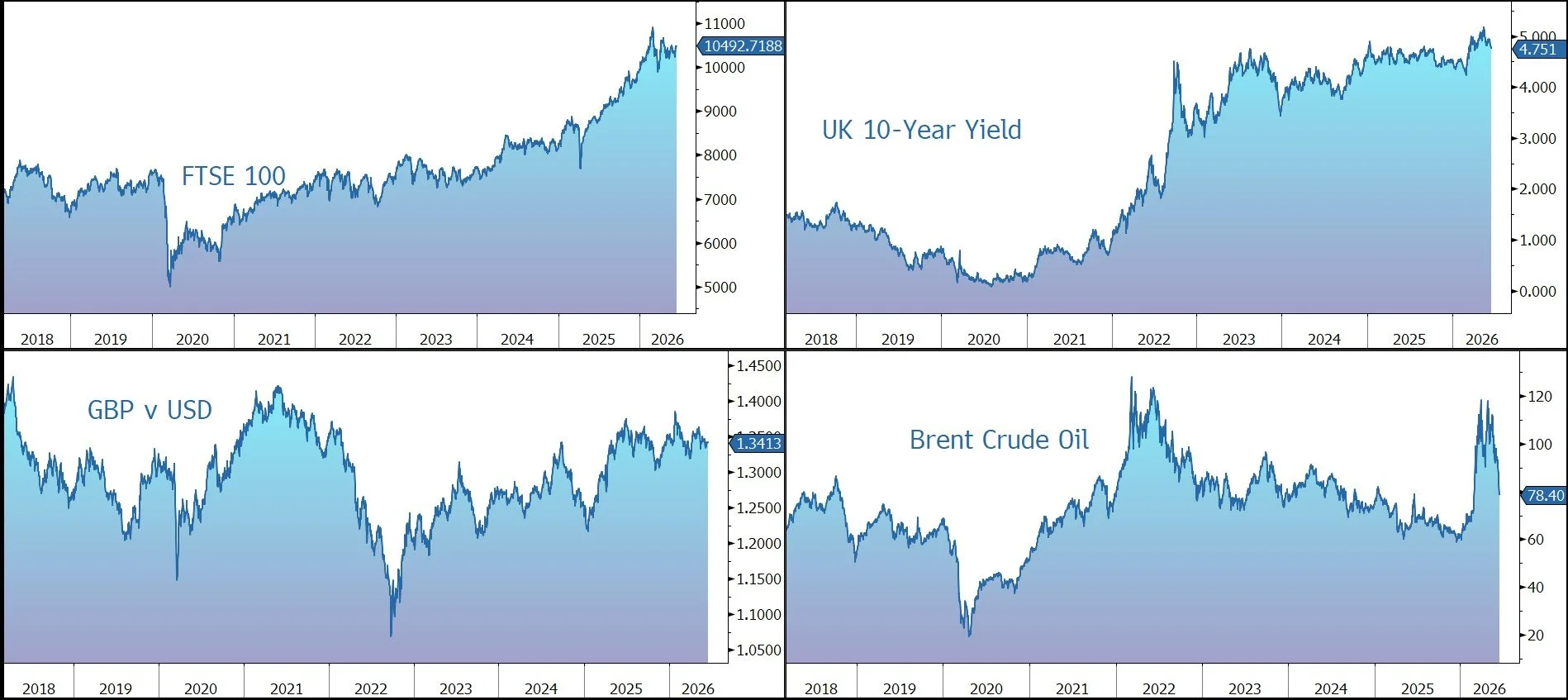

Contours of the US-Iran peace deal are emerging ahead of its expected signing on Friday, with a 14-point MOU outlining economic incentives for Tehran to end the war. Iran would be able to sell oil immediately, tap a $300bn development fund and eventually unlock frozen assets, though the timeline remains unclear. Separately, Tehran threatened a “harsh response” if Israel doesn’t stop Lebanon attacks, IRIB reported. France and Germany said they’re ready to help clear Hormuz, though officials remain wary of risking ships. Brent Crude moved down towards $78 a barrel.

The yield on the US 10-year Treasury trades at 4.43% as investors await the Federal Reserve’s latest policy decision, where it is widely expected to leave interest rates unchanged. The meeting will also be the first chaired by Kevin Warsh, although he is not expected to submit a ‘dot’ to the FOMC’s quarterly projections that outline individual officials’ expectations for the future path of interest rates. Gold held steady at $4,330 an ounce.

US equities saw some profit taking last night: S&P 500 (-0.6%); Nasdaq (-1.2%). SpaceX leapfrogged Amazon to become the fifth-largest publicly traded company. In Asia, equities were mixed: Nikkei 225 (+0.7%); Hang Seng (-0.7%); Shanghai Composite (+0.4%).

The FTSE 100 is currently down 0.2% at 10,478, while Sterling trades at $1.3420 and €1.1560. UK inflation unexpectedly held at 2.8% in May versus an estimate of 3%, with the core figure at 2.6%. The key services figure came in at 3.7% versus 3.2% in April and slightly above the economist survey. The 10-year Gilt yield slipped to 4.75%.

Source: Bloomberg

Fund News

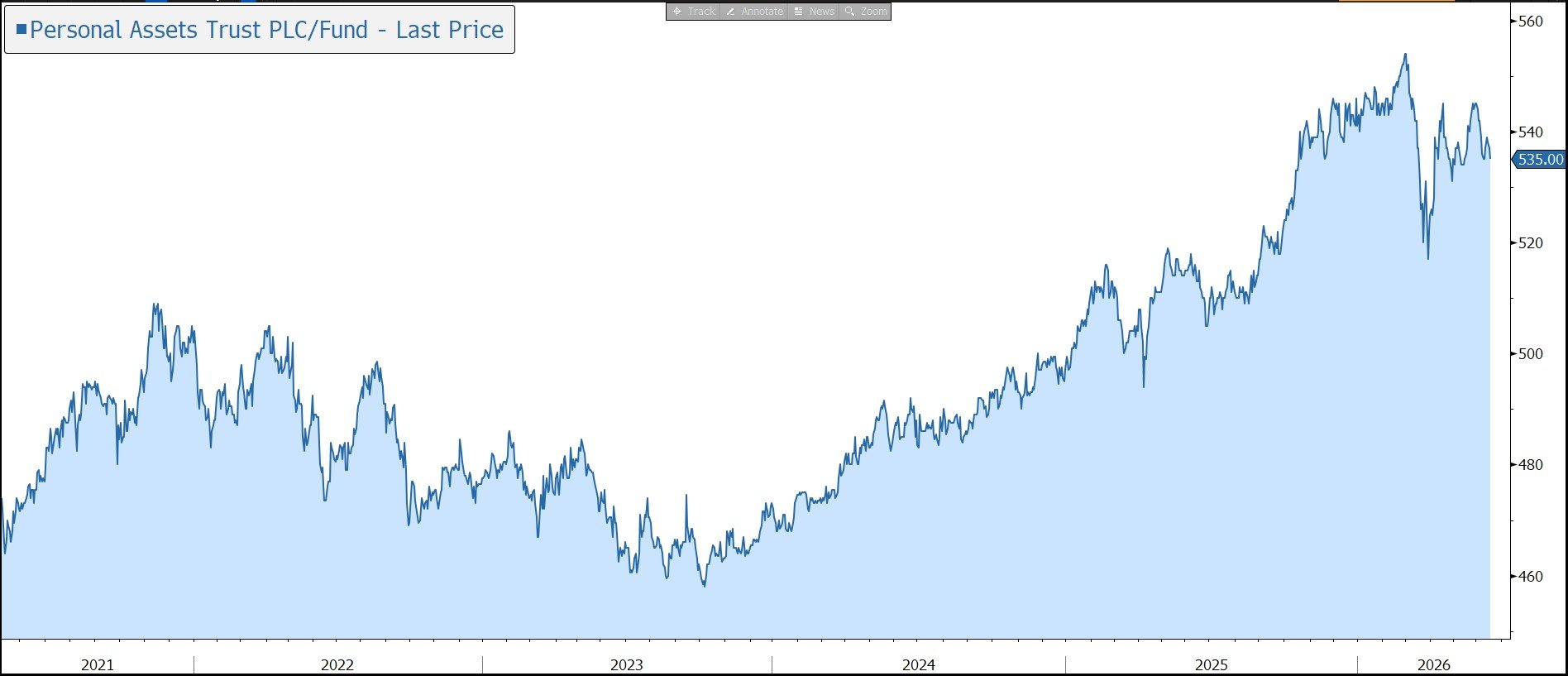

Personal Assets Trust PLC (PAT) is a £1.7bn UK-listed investment trust run by Troy Asset Management. The investment policy is to protect and increase (in that order) the value of shareholders’ funds per share over the long term. As a result, the fund can form a defensive cornerstone of an investment portfolio.

Since the appointment of Troy in 2009, the NAV (238.8%) and share price (223.7%) have outpaced the UK CPI inflation (64.4%). In the year to 30 April 2026, the NAV total return was 6.3%, while the share price total return was 6.2%. PAT is not constrained by a traditional benchmark like the FTSE All-Share Index; rather, it aims to achieve returns similar to equities over a market cycle but with significantly lower volatility. However, during the latest year, the fund lagged the FTSE All-Share Index, which rose by 25.2%. Returns rose in real terms, beating CPI of 2.8%.

The Manager prioritises the avoidance of permanent capital loss, which they consider the primary definition of risk, and on growing the real value of the Company’s capital over the long run. The portfolio is structured around a flexible, multi-asset approach, allowing the Managers to dynamically shift exposure across different asset classes depending on market conditions and perceived risk. This flexibility means the equity weighting can range drastically, demonstrating a high degree of tactical control.

PAT typically employs four main ‘pillars’ in its allocation, designed to offer both growth potential and resilience:

· High-Quality Equities - The largest component consists of large, well-established companies, often globally recognised brands (e.g., Alphabet, Unilever, and Visa). These firms are selected for their sustainable growth potential, strong cash generation, and resilience during economic downturns.

· Inflation-Linked Bonds - A significant portion of the trust is dedicated to inflation-linked fixed income, such as UK Index-Linked Gilts and US Treasury Inflation-Protected Securities (TIPS). This provides a substantial hedge against inflation risk and offers stability when nominal bond yields are low.

· Gold Bullion - Physical gold or gold-related investments are held as a defensive measure. Gold serves as a classic portfolio ballast, acting as a non-correlated asset that historically performs well during periods of high geopolitical tension or monetary instability.

· Cash and Cash Equivalents - The trust retains flexibility by holding cash, allowing the managers to deploy capital quickly when attractive valuation opportunities arise, particularly following significant market sell-offs.

In the year to 30 April, performance was described as ‘uninspiring’, at a time when stock markets were strong. However, beneath the surface of market indices (which were led higher by defence and financials in the UK and by tech and industrials in the US), there have been strong winners and severe losers. AI has been a persistent and dominant theme, with major casualties from a share price perspective in the software and information services sectors.

The equities allocation in aggregate contributed around a third of the Company’s return (+6% over the period). This was comprised of divergent parts, with the Company's largest holding, Alphabet, rising 140% and new holdings like Hubbell and Canadian National up 42% and 17% respectively. These were in part offset by poor performance from the likes of Diageo and Experian, both down 27% over the year. Three companies were sold from the portfolio during the year: American Express, Moody’s, and LVMH.

The conflict in the Middle East has pushed bond yields on both sides of the Atlantic higher, with the UK 10-year yield breaching the 5% level for the first time since 2008. The Company owns predominantly index-linked securities with modest duration for precisely the reason that it wants inflation protection but does not want exposure to duration if expectations for interest rates rise.

During the year, gold (+41%) contributed positively to performance. However, at the end of January, the Manager reduced the gold holding from 14% to 10% when the price reached over $5,100, a move that has proved timely as investors and central banks recently sold to access liquidity and in response to higher bond yields. The Manager remains bullish long term on gold and expects continued demand as both investors and central banks move away from the dollar.

The Company holds 10% of the portfolio in yen through short-dated Japanese Government Bonds. The Japanese currency is the cheapest it has been for four decades and the dollar has risen by 55% against the yen since 2020, moving well away from purchasing power parity. The Manager believes the holding will provide good diversification and an offset should stock markets become more risk averse. Repatriation of borrowings held overseas by domestic investors back into yen and political impetus to address the weak currency should also provide tailwinds.

The Manager believes markets appear remarkably complacent about the threats posed from the conflict in the Gulf. With all this in mind, the Company exited its financial year with a high level of liquidity – 54.8% at 30 April 2026. This included 30.6% in UK Gilts, UK index-linked bonds, UK cash, overseas cash, and net current assets and 24.2% in various classes of non-equity risk assets: 15.0% in US TIPS and 9.2% in Gold Bullion. The portfolio only holds 36% in equities. As opportunities emerge, the Manager will continue to add selectively to risk when paid to take it.

To ensure liquidity and investor confidence, the trust operates a robust Discount Control Mechanism. This ensures that the shares trade close to NAV by issuing new shares when demand is high (at a slight premium) and buying back shares when the share price falls below NAV (at a slight discount). In the latest year, the Company bought back 10.4m shares at a cost of £57m and issued 5.3m shares from Treasury for £32m. This stability in pricing is a major feature, distinguishing it from many other investment trusts which can often trade at wide discounts.

The trust targets consistent, sustainable dividends, compatible with its primary goal of capital protection. For the financial year to end-April 2026, the Company paid 5.6p per share in four quarterly payments, amounting to a yield of just over 1%. It is the Board’s intention, barring unforeseen circumstances, that a first interim dividend for the year ended 30 April 2027 of 1.4p will be paid in July 2026.

Source: Bloomberg