Morning Note: Market News and an Update from McCormick.

Market News

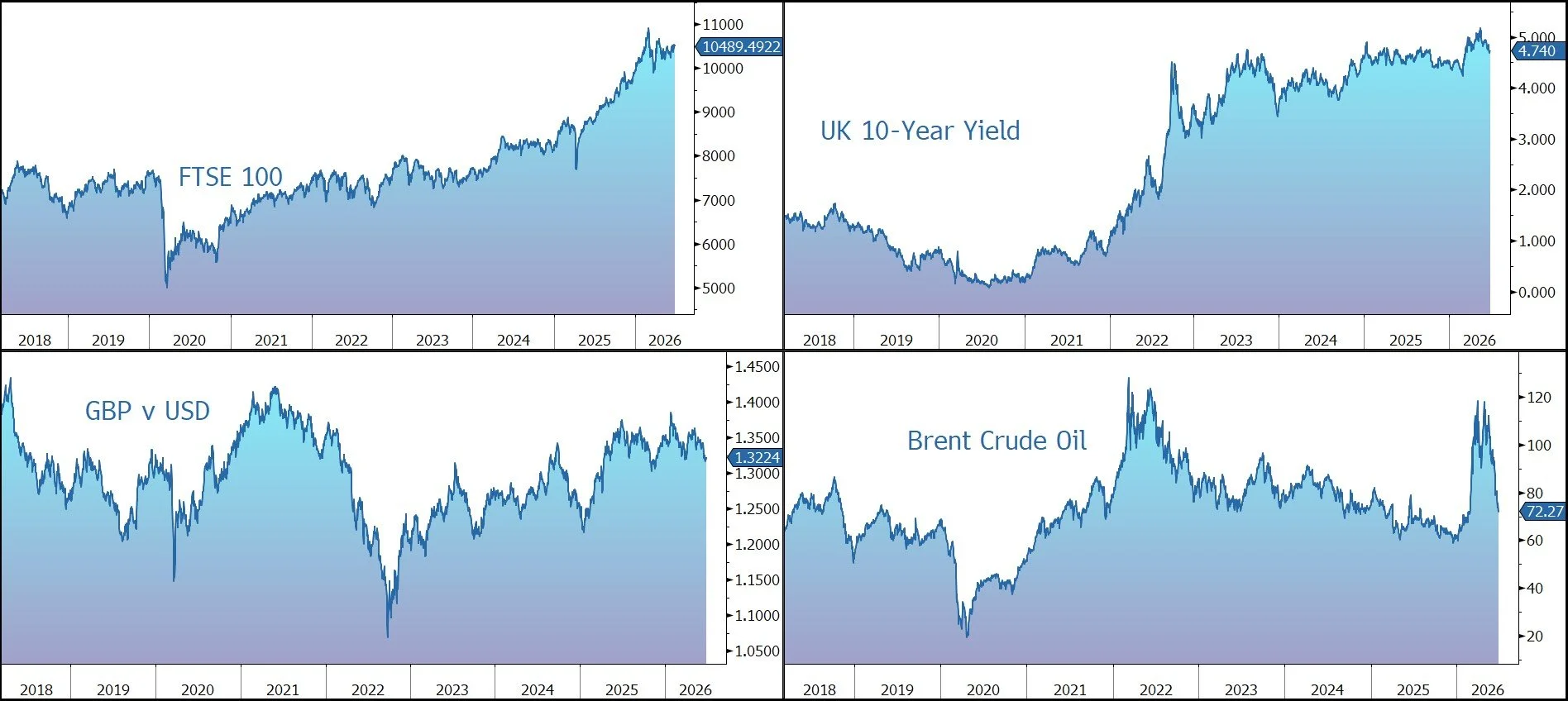

US equity-index futures rose after reports that the US and Iran backed away from a fresh escalation of their conflict, easing concerns over the fragile ceasefire underpinning peace talks. The rally came after Axios reported the US and Iran agreed to halt strikes and meet this week in Qatar to resume talks over the Strait of Hormuz and other issues to end the war, citing an unidentified US official. Brent Crude trades at $72.50 a barrel.

In Asia this morning, equities also kicked off the week on a positive note: Nikkei 225 (+0.2%); Hang Seng (+2.0%); Shanghai Composite (+1.0%). South Korea’s Kospi index swung to a gain after the nation unveiled an ambitious plan aimed at cementing its status as a technological powerhouse. Samsung and SK Hynix plan to build two chip fabs apiece as South Korea aims to double its DRAM production capacity over the next five years.

Google capped Meta’s use of its Gemini AI models because it could not provide enough computing capacity to meet its demand, the FT reported.

The FTSE 100 is currently 0.2% lower at 10,489, while Sterling trades at $1.3225 and €1.1590. BT and Verizon will combine their international enterprise businesses in a 50:50 JV that will have about $4bn in annual revenue.

The Fed’s Tom Barkin said inflation is too high, but there are tentative signs that price pressures may moderate soon. The yield on the US 10-year Treasury is currently 4.38%, while gold trades at $4,060 an ounce.

Prime minister-in-waiting Andy Burnham, in his first major speech since confirming his intention to succeed Keir Starmer, will pledge to hand more decision-making powers to local authorities, overhaul procurement, and tackle youth unemployment. The 10-year Gilt currently yields 4.75%, well below the recent peak of almost 5.2%.

Source: Bloomberg

Company News

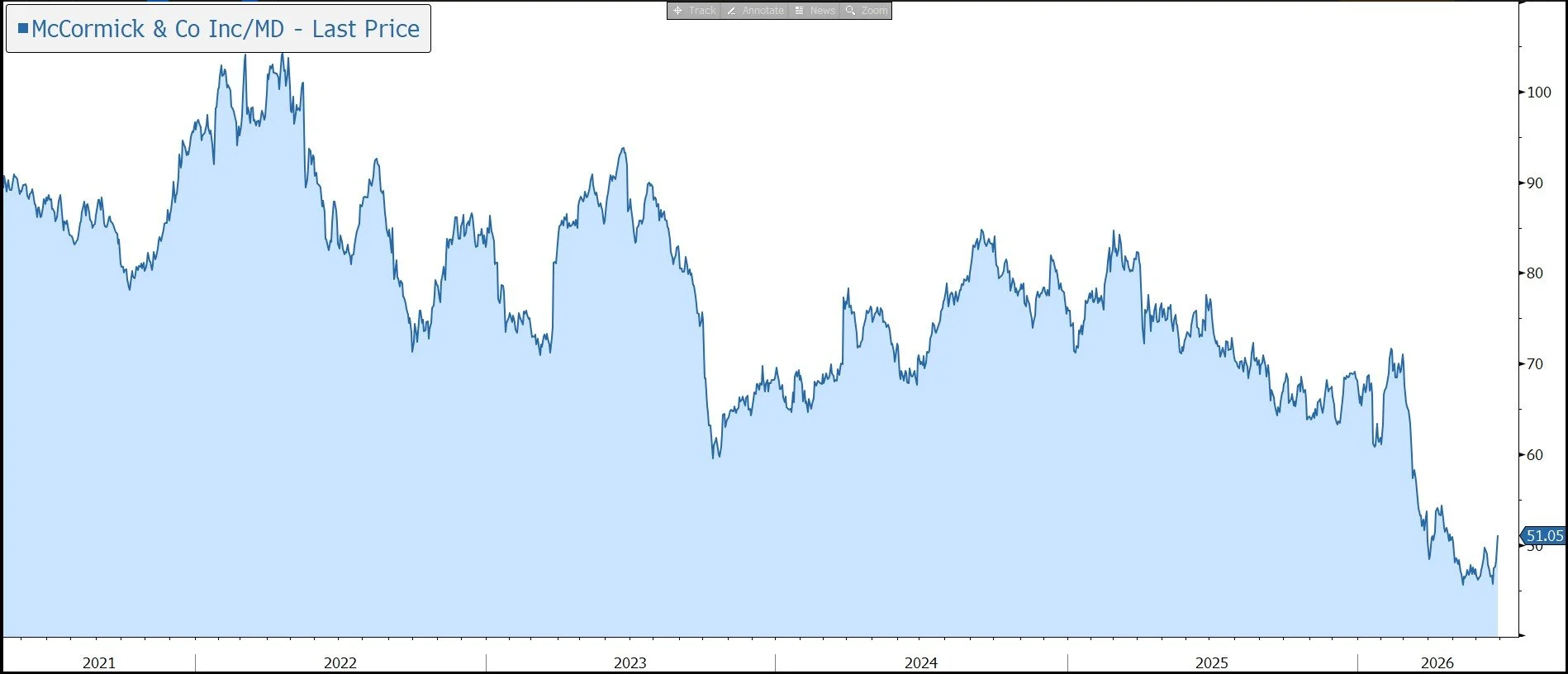

At the end of last week, McCormick released results for the three months to 31 May, the second quarter of its financial year to 30 November 2026. The figures came in above market expectations, driven by strong demand for its spices and seasonings as consumers cook more at home amid economic uncertainty. The company highlighted it is making strong progress on integration planning for its proposed combination with Unilever Foods and reaffirmed its full-year guidance. In response, the shares were marked up by 5%.

McCormick is a US-listed global leader in ‘flavour’ generating $7bn in annual sales across 150 countries and territories. The company manufactures, markets, and distributes herbs, spices, seasonings, condiments, and flavours to the entire food and beverage industry including retailers, food manufacturers, and foodservice businesses. Leading brands include McCormick, French’s, Schwartz, and Frank’s. In order to reduce costs, the company is undertaking a Comprehensive Continuous Improvement (CCI) programme.

In March, the company announced the agreement to combine McCormick with Unilever’s Foods business to create a pre-eminent global flavour-focused company operating in attractive, high-growth categories, with $20bn of sales and a 21% operating margin. In addition to the McCormick brands, the deal adds household names such as Knorr, Hellmann’s, and Marmite. Work is already underway to support the delivery of $600m of annual run rate cost synergies (net of growth reinvestments) and incremental cost and revenue synergies of $100m. This process is made easier because 80% of Unilever Foods operates as a standalone, while the top-10 markets represent 75% of combined company sales.

The deal is expected to close in mid-2027 and is subject to McCormick shareholder approval and the receipt of required regulatory approvals. The company expects to announce the location of a secondary listing on a European exchange by the end of July 2026. The transaction is expected to be accretive to McCormick’s net sales growth rate, operating margin, and adjusted EPS. With these results, the company highlighted it is making strong progress on integration planning for the proposed combination and remains confident in delivering the expected strategic and financial benefits.

The company’s latest quarterly results demonstrate the continued strength and resilience of the business in a dynamic operating environment.

Net sales increased 16.7% to $1.94bn, slightly better than market forecast of $1.91bn. Stripping out the favourable impact from currency (+2.7%) and M&A (+12.3%, mainly McCormick de Mexico), organic sales growth was 1.7%. Growth was made up of price increases of 2.2%, offset in part by a 0.5% decline in volume/product mix.

Revenue is split between two divisions. Firstly, Consumer (60% of sales), which includes spices & seasonings, recipes mixes, and condiments & sauces. Organic sales increased 0.8% in the quarter, driven by a 3% increase from price partially offset by a 2% decline in volume/product mix. The company gained share in spices and seasonings, recipe mixes, mustard, and hot sauce in select markets, but saw softening consumption trends in US spices and seasonings.

Secondly, Flavour Solutions (40% of sales), which includes flavours, branded foodservice, custom condiments, and coatings & bulk spices. Organic sales increased 2.9% in the quarter, driven equally by both price and volume/product mix. The business saw accelerated volume growth in flavour and branded foodservice.

Gross profit margin rose by 270 basis points to 40.2%. The expansion was driven by a contribution from the acquisition of McCormick de Mexico, the impact of a $28m tariff refund, pricing, and cost savings, partially offset by higher commodity costs and costs related to the Middle East conflict. The underlying GM increase was 130 basis points, just above the full-year expectation of 100-120 basis points.

Adjusted operating income rose by 30% to $336m, with the underlying margin up 180 basis points to 17.4%. Adjusted EPS increased by 16% to 80c, well above the consensus estimate of 69c. A quarterly dividend of 48c was declared. The company has spent $75m on capital expenditure in the year to date to leave net debt of $4.6bn at the end of the quarter. McCormick is still positioned to reduce its financial leverage ahead of the Unilever Foods combination.

Looking to the full year, the company expects to sustain the momentum in Flavour Solutions and increase reinvestment to improve Consumer volume trends and organic sales. Guidance for the full year was reaffirmed: sales growth (12%-16% at constant currency); organic sales growth (1%-3%); adjusted operating income (15%-19%), and adjusted EPS (1%-4%).

Source: Bloomberg