Morning Note: Market News and an Update from Kingfisher.

Market News

Optimism around a potential de-escalation in Middle East tensions remains fragile. The Wall Street Journal reported that US allies in the Persian Gulf are inching toward joining the fight against Iran. Adding to the downbeat tone, Iran’s deputy speaker ruled out talks with the US, echoing similar comments from other officials in the regime. Pakistan is making a push to mediate talks between the US and Iran in Islamabad, people familiar said.

The shift marked a reversal from yesterday, when stocks rose and oil slumped after President Trump signalled a delay in strikes on Iranian energy assets. The conflict showed few signs of easing and the Strait of Hormuz — crucial for the flow of oil from the Middle East — remained effectively shut with only a trickle of vessels making their way through.

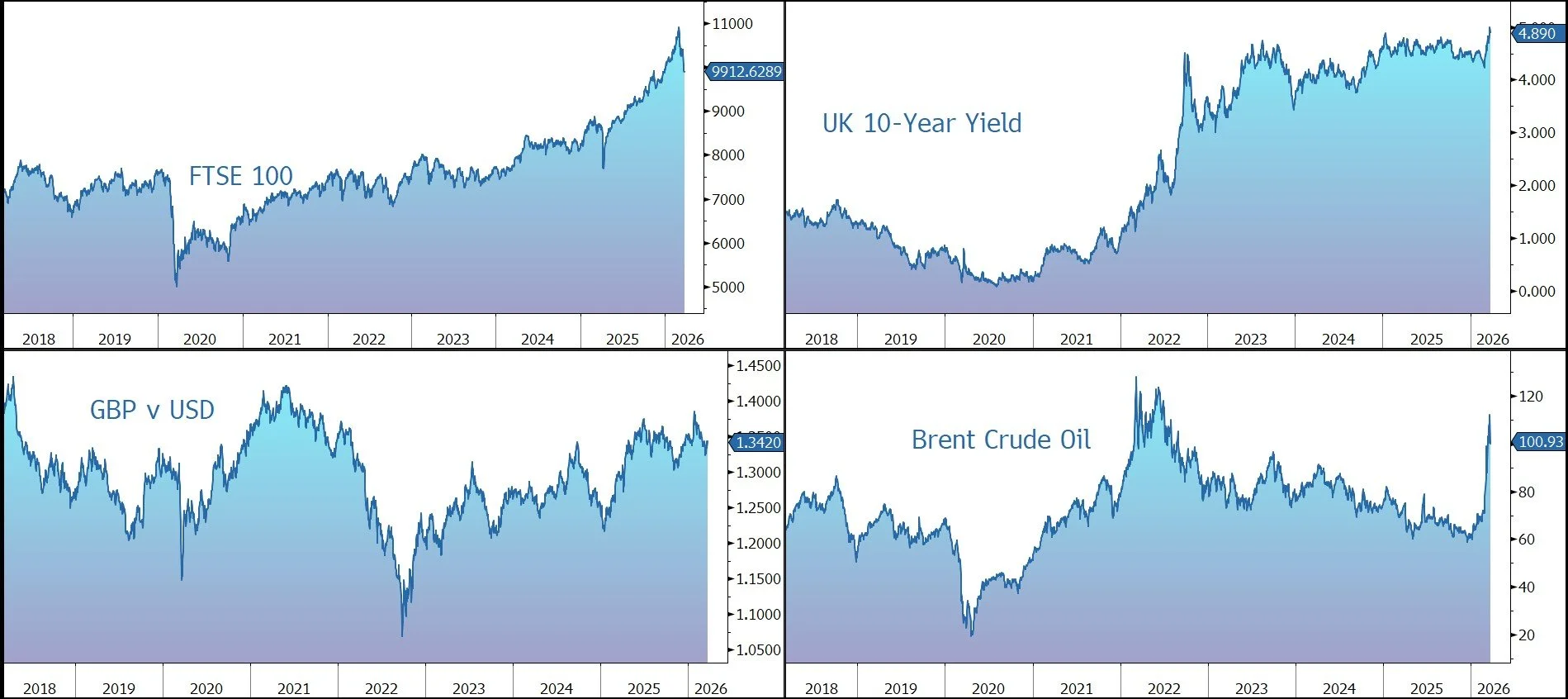

Brent Crude is currently trading slightly higher at $101 a barrel – this follows yesterday’s 10% plunge – while 10-year Treasury yields are 4.35%. Gold is little changed this morning at $4,400 an ounce. Chinese banks are experiencing system failures due to surging volumes in gold investment products as investors buy on dips, according to China Securities Journal.

US equities closed higher last night – S&P 500 (+1.2%); Nasdaq (+1.4%) – and are currently expected to open up slightly this afternoon. JPMorgan is said to be offering clients a new CDS basket tied to hyperscalers to hedge AI debt risk.

In Asia this morning, markets played catch-up with yesterday’s gains elsewhere: Nikkei 225 (+1.4%); Hang Seng (+2.6%); Shanghai Composite (+1.8%). Alibaba unveiled a new chip for agentic AI and inference computing.

The FTSE 100 is currently 0.2% higher at 9,913, while Sterling trades at $1.3415 and €1.1565. The 10-year Gilt yield has pulled back to 4.85%, after surging to almost 5.10% yesterday, its highest since July 2008.

Source: Bloomberg

Company News

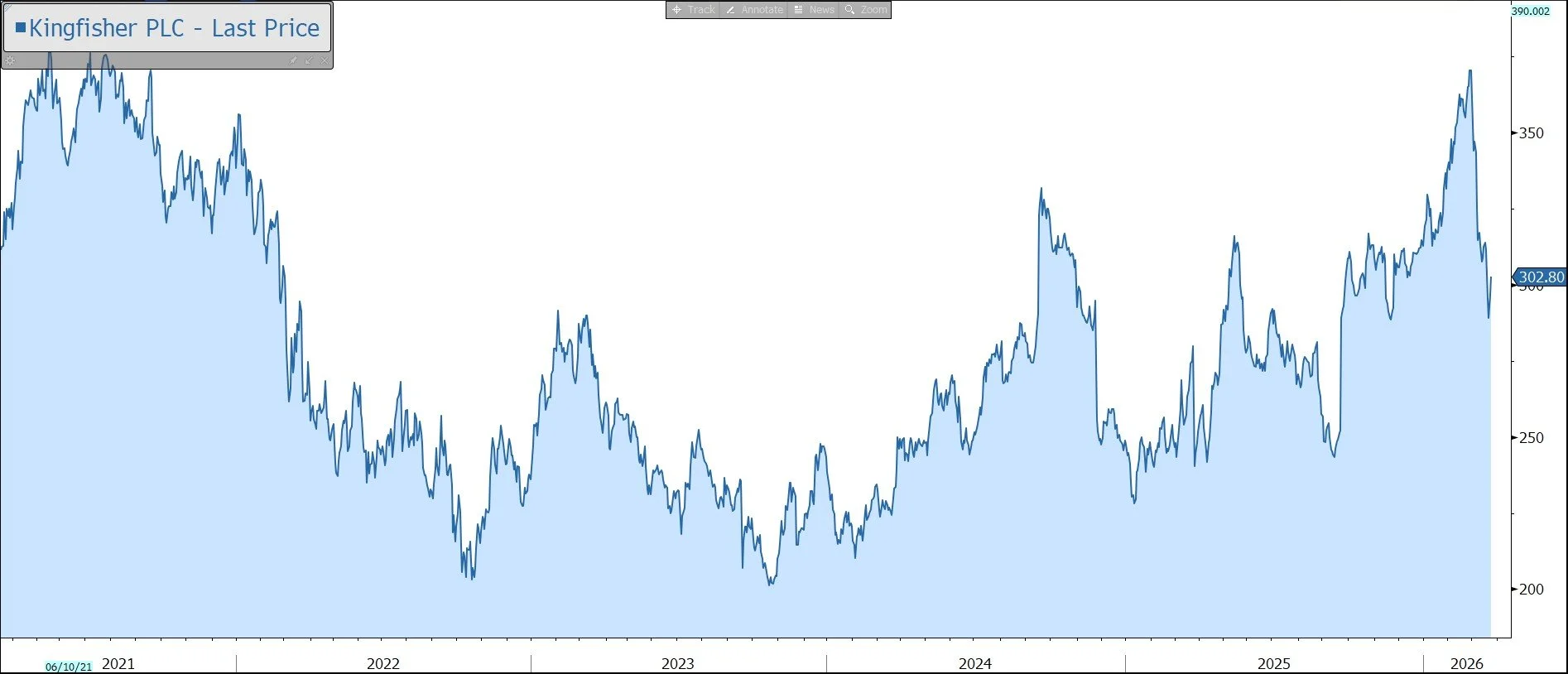

Kingfisher has this morning released results for the financial year to 31 January 2026, which were slightly better than expected driven by strategic progress, market share gains, and financial discipline. The dividend has been maintained and a new share buyback programme launched. In response, the shares have been marked up by 1% in early trading.

Kingfisher is a pan-European DIY chain with around 1,700 stores across brands such as B&Q, TradePoint, Screwfix, and Castorama. The European home improvement market is £235bn across a customer base of 320m homes. Growth is expected to be driven by population growth, urbanisation, and the need to repair an ageing housing stock. This is being helped in part by working from home and the focus on energy efficiency.

The company’s sales are made up of Core categories (67% of the total) which include the sales from non-seasonal products across all categories, other than 'big-ticket' sales. Big-ticket sales (15%) include the sales of kitchen, bathroom & storage products. Seasonal category sales (18%) include the sales from certain products within the group’s outdoor, electricals, plumbing, heating & cooling (EPHC), and surfaces & décor categories.

The group’s medium-term financial priorities are focused on growth, cash generation, and higher returns to shareholders. Retail space is expected to grow by 1.5%-2.5% each year. The ambition for trade sales is to reach £5bn in the medium term. The group is targeting sales growth ahead of its markets, adjusted PBT growth faster than sales growth, and free cash flow of more than £500m p.a. from FY26/27. The group intends to maintain an efficient capital structure, with surplus capital to be returned via share buybacks or special dividends.

In the near term, the company highlights that mixed consumer sentiment and political uncertainty remains, as do ongoing cost pressures.

During the year to 31 January, reported sales grew by 0.2% at constant currency to £12.95bn. On a like-for-like (LFL) basis (which includes stores that have been open for more than a year and excludes the impact of currency and portfolio changes) sales rose by 1.1% on an underlying basis driven by volume and transaction growth.

Group trade sales now represent 30% of revenue and grew by 23% excluding Screwfix (+12% with Screwfix), driven by our expanding trade proposition across banners. Total e-commerce sales rose by 20% ex-Screwfix (+11% including Screwfix) and now account for 21% of sales, vs. a 30% ambition.

Kingfisher UK & Ireland LFL sales rose by 3.3%, with B&Q and Screwfix up 3.3% and 3.2%, respectively. Growth was driven by trade and e-commerce initiatives, product innovation, strong seasonal sales, and transference from the closure of Homebase stores.

Outside of the UK, performance was mixed. Kingfisher France LFL sales fell by 2.2%, with Castorama -2.2% and Brico Dépôt -2.3%. Poland fell by 1.1%, while the Other International division saw LFL sales grow 8.0%.

The company enjoyed market share gains in the UK (+4% at B&Q and +4.5% at Screwfix), France, and Spain, while Poland was broadly in line with the market. This reflects the growth of the digital ecosystem, increased share of wallet from trade customers, and the opening of 41 net new stores.

The group entered the year with significant cost headwinds consisting of wage inflation, higher UK employer national insurance contributions, increased social taxes in France and the new packaging fees in the UK. Against this backdrop, the group remained disciplined on managing costs and cash.

The group’s gross margin rose by 80 basis points to 38.1%, reflecting the leveraging Kingfisher’s buying and sourcing scale, growth from marketplace and retail media, AI driven promotional effectiveness, improved inventory management and clearance activity, and banner mix. The adjusted retail profit margin increased by 30 basis points to 5.7%, driven by gross margin and operating cost initiatives.

Adjusted pre-tax profit, which excludes the impact of transformation P&L costs and exceptional items, rose by 6% to £560m, ahead of guidance to be at the ‘upper end’ of its £480m-£540m range.

The group generated free cash flow of £512m, up 0.1%, versus the guidance range of £480m-£520m and was driven by earnings growth, receipts of tax settlements relating to prior years and effective working capital management, while increasing capex investment.

As a result, net debt fell by 7% to £1,878m, with gearing falling to 1.4x net debt to EBITDA, well below the medium-term target ceiling of 2.0x.

The dividend was held at 12.4p, equating to a yield of 4%. Earlier in the month, the company completed a £300m share buyback programme and has today announced the commencement of a new £300m programme.

Looking forward to the full financial year to 31 January 2027, the group expects adjusted PBT of £565m-£625m, while free cash flow is expected to reach £450m-£510m.

Source: Bloomberg