Morning Note: Market News and an Update from Diageo.

Market News

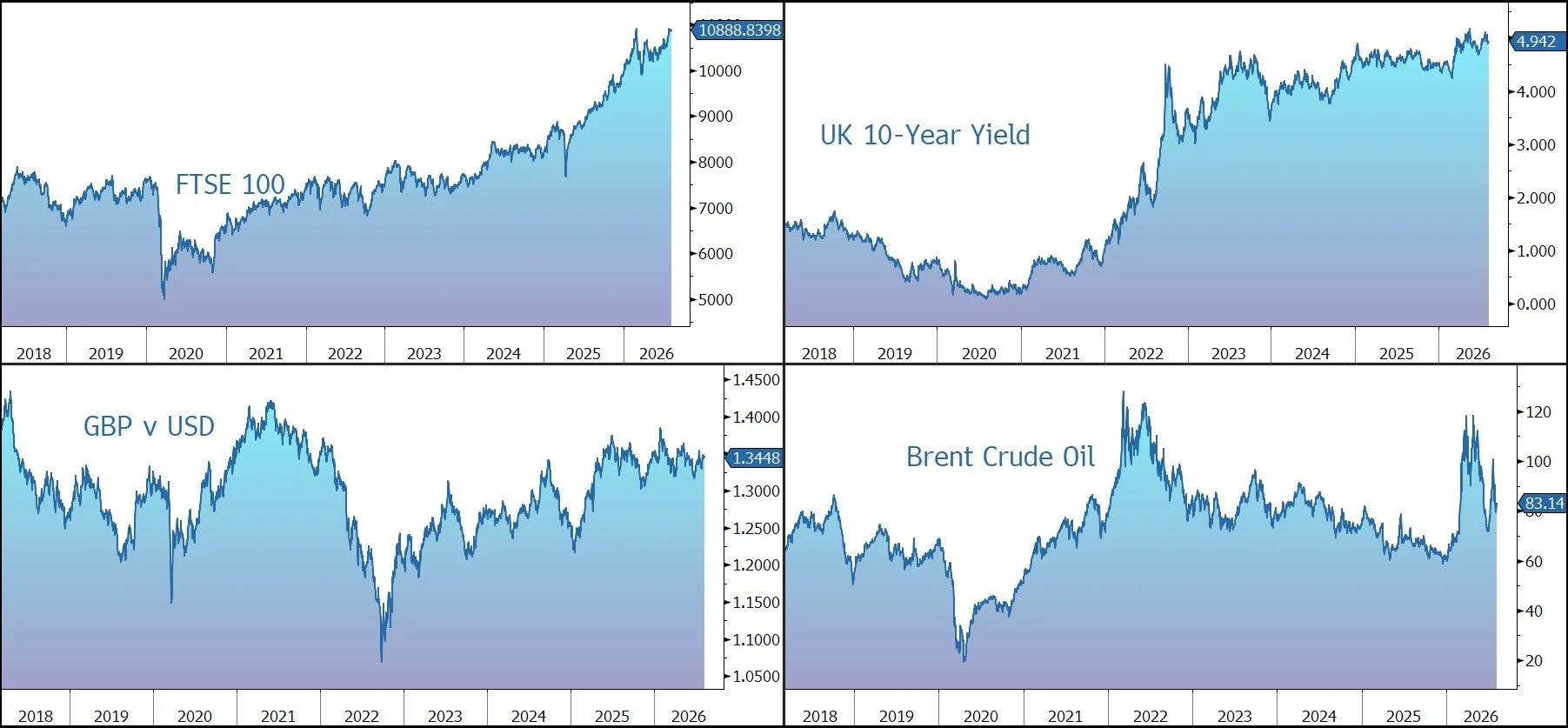

Brent crude moved up to $83.50 a barrel as prospects for a lasting agreement to reopen the Strait of Hormuz remained elusive. Iran reportedly struck “hostile targets” in the Strait of Hormuz overnight, with Tehran seeking to exclude US and Israeli ships from the waterway in a deal brokered via Oman.

Bonds fell on inflation concerns as traders awaited the US jobs report for clues on the path of interest rates. Payrolls are expected to rise 80,000 in July, while Bloomberg Economics predicts a softer 65,000 gain. The unemployment rate is forecast to hold at 4.2%. The yield on the US 10-year Treasury rose to 4.68%.

Gold continued its recent recovery and currently trades at $4,285 an ounce. Data from clearing institutions showed that institutional investors in China continued to build long positions in gold-backed assets as a hedge against volatility in technology stocks, with demand also supported by continued central bank buying.

The yen (158.50 vs. the dollar) continued to give up its intervention-driven gains, fueling speculation authorities may step in again. The US informed the ECB of its euro sales to support the yen only after the intervention.

Equities are relatively stable as investors wait for the jobs data, both in the US last night – S&P 500 (-0.2%); Nasdaq (-0.1%) – and in Asia this morning: Nikkei 225 (-0.1%); Hang Seng (+0.4%); Shanghai Composite (+1.0%); Kospi (-0.6%).

The FTSE 100 is currently 0.2% higher at 10,888, while Sterling trades at $1.3450 and €1.1670. UK house prices were flat in July, with annual growth slowing to its weakest pace since late 2023 as affordability pressures and higher mortgage rates continued to weigh on the market. According to the Lloyds (formerly Halifax) house price index, the average UK property price was unchanged month-on-month at £299,253 in July. On an annual basis, house prices rose 0.1%, slowing sharply from 0.7% in June.

Source: Bloomberg

Company News

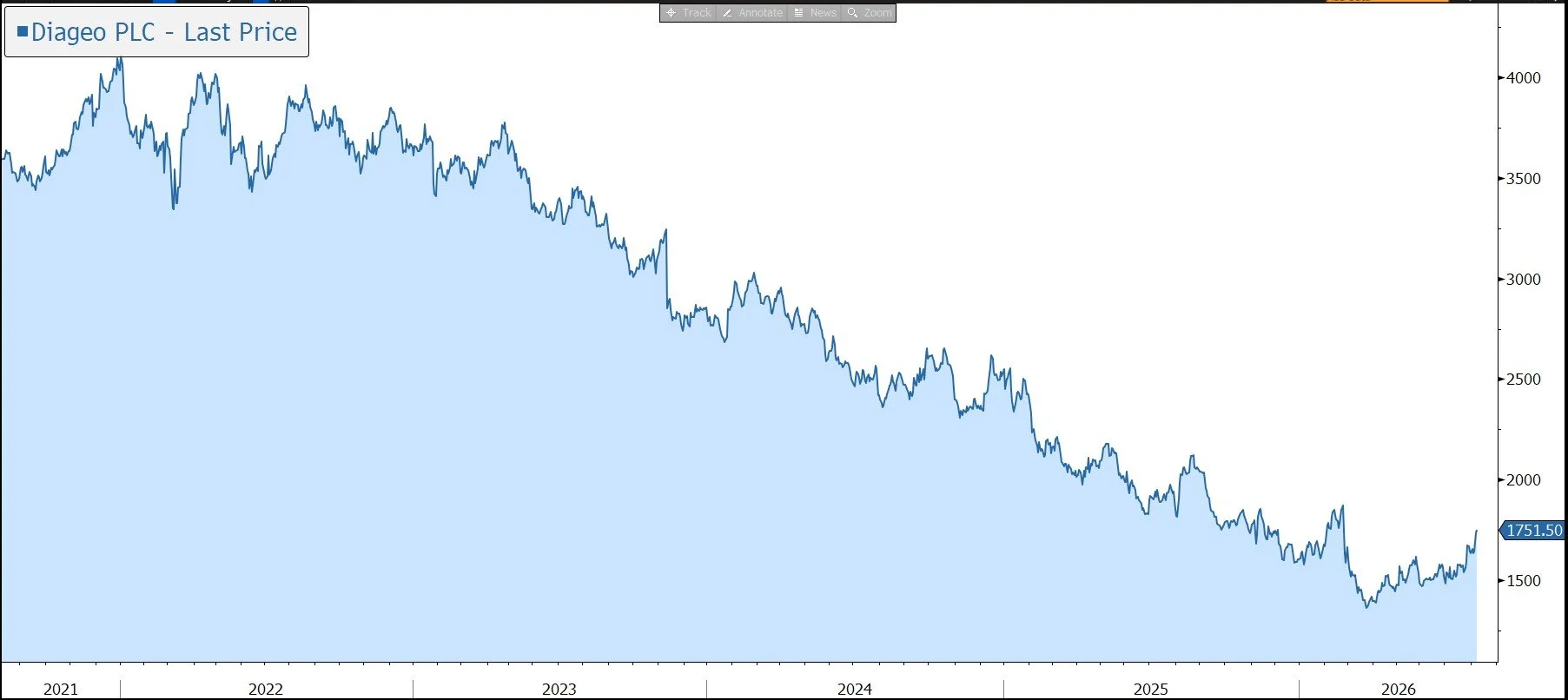

Yesterday Diageo released results for the financial year to 30 June 2026, following which it detailed its new strategy at a Capital Markets Day. The figures were pretty much in line with market expectations and guidance for the current financial year (FY2027) is realistic and achievable. In a broad strategic reset, the new CEO announced a $1bn cost savings plan as Diageo looks to optimise its operating framework and supply chain. There are risks: turning around the North America business won’t be easy and implementation of the restructuring plan could be disruptive. However, there was relief that the company didn’t deliver an unexpected secondary shock – there were fears of a margin reset – but instead set out a clear, realistic growth target without further negative surprises. In response, the shares were marked up by 6%.

Diageo is a leading global drinks company, with a portfolio of iconic brands including Johnnie Walker, Smirnoff, Captain Morgan, Baileys, Tanqueray, and Guinness. The company owns 13 billion-dollar brands across a broad range of categories. The group is an integrated operator, producing and supplying drinks at a variety of price points across strong global distribution routes. The company has been positioned to benefit from the trend towards premiumisation – including its 34% stake in Moet Hennessy, the group generates more than 60% of its sales from high margin, premium brands. Diageo also has a strong presence in under-penetrated emerging markets, where the number of people of legal purchasing age is set to increase by over 600m by 2030. Wealth is also increasing in these regions, with the middle class expanding, and consumers shifting from local products to higher-margin international brands.

In the near-term, however, the global industry environment has been challenging, with headwinds from the impact of weight-loss drugs on alcohol consumption, warnings from health authorities, Gen-Z moderation, and cannabis cannibalisation. However, the data the company is currently seeing shows penetration and frequency of spirits consumption as broadly stable, including among younger cohorts, with the more meaningful change being a reduction in servings per occasion rather than outright disengagement from the category. This implies that the biggest consumption headwind may be cyclical, not structural, and that an upturn in consumer confidence, particularly in western markets, could be an inflection point for the sector.

Yesterday afternoon, new CEO Dave Lewis – ex Tesco and Unilever – set out the company’s new strategy. The three priorities outlined earlier in the year – relevant brands in competitive category strategies, improved customer focus, and a more agile and competitive operating framework – are already serving the company well and lay the foundation for the new strategy.

The revised operating framework is being rolled out across Diageo and the changes are significant. The organisation is being vastly simplified, with less duplication and improved benefits of scale. There is a focus on improved supply chain capability. The company stressed that this is an organic turnaround, with no need for M&A.

There are two strategic battlegrounds:

· Spirits and RTDs (ready to drink) – the company will manage both within each brand. It will retain its focus on premiumisation but will also broaden its reach to serve more customers on more occasions. Some brands are being positioned at lower price points, to broaden the customer base, so the portfolio is fit for all stages of the economic cycle. However, the investment will not just be in price, but also format size and other competitive initiatives.

· Brewing through Guinness - the company remains excited about the growth potential in Guinness, with accelerated investment to leverage this opportunity more fully.

By 1 September, the company will have implemented 90% of the new structure, leaving only parts to Europe to complete. The company will operate through 23 country and country cluster organisations, reporting into five regional divisions (North America, Latin America & Caribbean, EMEA, Asia Pacific, and India). As a result, SG&A/overheads are expected to drop to 10.5% of sales.

In total, Diageo expects to generate $1bn in savings over the next three years from the operating framework as well as further work on supply chain. The operating framework redesign is expected to deliver $850m of savings, with 40% in FY2027 and the balance in FY2028. The company also expects $150m of savings from supply chain initiatives, with 25% in FY2027 and the balance in the following years. Restructuring costs related to both programmes will total $1.2bn; $1.1bn for the operating framework, of which $752m was incurred in FY2026, and $100m for the supply chain savings expected to be incurred in FY2027. These savings provide the firepower to invest in marketing and US distribution without the need to reduce operating profit.

In addition to guidance for FY2027 (see below), the company has introduced guidance for the medium term through to FY2029. The company expects a CAGR of:

· low-single-digit organic net sales growth, accelerating over the period as Diageo stabilises and grows share in North America.

· Sales growth by region will be: North America (-2% to 0%), Latin America & Caribbean (4%-6%), EMEA (2%-4%), Asia Pacific (0% to +2%, held back by China), and India (4%-6%). Guinness is expected to grow faster than the premium beer average of 1%-3%.

· mid-single-digit organic operating profit growth, reflecting the benefit of savings and more favourable mix over the period.

· attractive EPS growth ahead of organic operating profit growth, on a currency neutral basis.

· capital investment is being raised to $1.25bn for the next three years.

· cumulative free cash flow of $8bn over the three years after $850m of exceptional cash costs, mainly relating to the operating framework changes.

The target is to exit FY2029 at 2.5%-3.0% sales growth. Importantly, there was no margin reset. The gross margin is expected to remain above 60%, with the focus on growing gross profit dollars. Advertising & promotion spend is expected to rise to 16% of sales, slightly above the current reduced level, following the removal of waste and duplication. Operating margins are expected to expand as operating expenses fall.

The company also published its results for the financial year to 30 June 2026. Reported net sales rose to 3.0% to $19.6bn. Organic net sales (which exclude M&A and currency movements) fell by 2.0%, versus guidance to be down by 2%-3%. The decline was driven by 0.4% fall in organic volume and a 1.6% negative price/mix, with the latter primarily the result of adverse mix due to US Spirits performance and weaker results in Chinese White Spirits.

By brand, growth was driven by Guinness (+12% organic sales growth), Buchanan’s (+12%), and Johnnie Walker (+2%).

North America, the group’s largest market (43% of profit), remains the biggest challenge, where market conditions are soft and Diageo’s offer needs to be more competitive. Actions are already underway to address this. During the year, organic sales fell by 8.4%, including a 11.5% decline in US Spirits due to tough year-on-year comparatives. The main culprit was Tequila, where net sales declined 21.%, driven by both Don Julio and Casamigos, reflecting a softer category and increased competitive intensity.

Asia Pacific also declined (-6.3%), with Greater China down 35% driven in part by the consequences of government policy in Chinese white spirits. Elsewhere, the company generated growth in Europe (+3.4%, led by Great Britain and Türkiye), Latin America and Caribbean (LAC, +7.7%), and Africa (+13.3%).

Cost savings from the original Accelerate programme over-delivered on guidance, with $540m of savings secured in the year. Group operating profit rose by 2.0% in organic terms to $5,683m, versus guidance to be flat to up low-single-digit. The underlying margin rose by 116 basis points in organic terms to 28.9%, as cost savings were partly offset by adverse mix and tariffs.

Restructuring charges in FY2026 of $0.9bn included $752m costs for the implementation of the group’s new operating framework (representing 70% of the total cost) with the balance related to supply chain agility and Accelerate costs. During the year, the company also took impairment charges of $1.5bn related largely to Türkiye due to the impact of hyperinflationary accounting and change in pricing in market, as well as the write down of the Don Papa brand and certain other smaller brands.

Free cash flow rose by 17% to $3.2bn, ahead of the guidance of $3bn, driven by lower capex (-24%) and maturing stock investment, along with lower year-on-year tax payments, partly offset by an adverse creditor movement and also the payment of termination fees to Moët Hennessy. As expected, free cash flow included a $100m one-off working capital impact from inventory build ahead of the SAP S/4 HANA ERP system implementation in early FY2027.

Financial gearing ended the year at 3.1x net debt to EBITDA, just above its target range of 2.5x-3.0x. The company now expects to return to the mid-point of its target range at the end of FY2027, a year earlier than previously expected. This will be helped by disposals. The sale of the company’s stake in East Africa Breweries for $2.3bn remains on track to complete in calendar H2 2026. The disposal of Royal Challengers Bengaluru cricket team by United Spirits Limited (56% owned by Diageo) is progressing as planned. Diageo is expected to receive a special dividend from USL for its share of the after-tax proceeds.

In the meantime, and in order to create more financial flexibility, Diageo has rebased its dividend – a saving of $1.2bn. The company is committed to growing shareholder distributions over time and is targeting a 30%-50% payout policy going forward, with a minimum floor set for the dividend of 50c p.a., down 52% versus FY2025. For FY2026, a dividend of 50 cents has been declared, equal to a yield of 2%. Looking forward, the company will review the gearing target range annually with an eye on whether to initiate increased shareholder returns.

Guidance for the financial year to June 2027 has been initiated:

· Organic sales growth is expected to be broadly flat, with North America down mid-single-digit. This assumes that the overall North America market is down 3% and Diageo improves share performance compared to FY2026.

· Organic operating profit growth in the low single digits. This is better than the consensus of +0.6%. The guidance includes 40% of the $850m cost savings from the operating framework changes and 25% of the $150m supply chain savings.

· free cash flow of $2bn after $800m of exceptional cash costs related to the operating framework changes and $50m exceptional cash costs related to the supply chain savings programme.

Source: Bloomberg