Morning Note: Market news and an update from Deere.

Market News

The CME halted trading of commodities futures and options due to a cooling issue at a data centre. Treasuries and S&P 500 futures were also affected, traders said, as well as platforms including EBS.

Gold moved up to $4,160 an ounce overnight and is poised for its fourth monthly gain on federal reserve rate-cut optimism. Brent Crude is headed for its longest run of monthly losses since 2023 ahead of this weekend’s OPEC+ meeting. In the mining sector, Anglo American’s proposed takeover of Teck cleared Canada’s national security test, the Globe and Mail reported.

In Asia this morning, equity markets were little changed: Nikkei 225 (+0.2%); Hang Seng (-0.3%); Shanghai Composite (+0.3%). In China, Four Vanke onshore yuan bonds were suspended from trading after a sharp plunge reviving fears of a property crisis.

The FTSE 100 is currently 0.2% higher at 9,703, while Sterling trades at $1.3210 and €1.1415. The UK dropped a key measure on unfair dismissal from its workers’ rights bill to allay businesses’ concerns. Bank of England rate-setter Megan Greene played down hopes that a cut to energy bills in Wednesday’s budget will help ease the threat from sticky inflation.

The FT reports the UK government is considering the expansion of the short-term debt market in a ‘radical’ borrowing shift. At present, the average maturity is 14 years, far longer than other countries. The aim to is lower its interest bill as demand for long-term paper from pension funds recedes. 10-year gilt yields held at 4.45%.

Source: Bloomberg

Company News

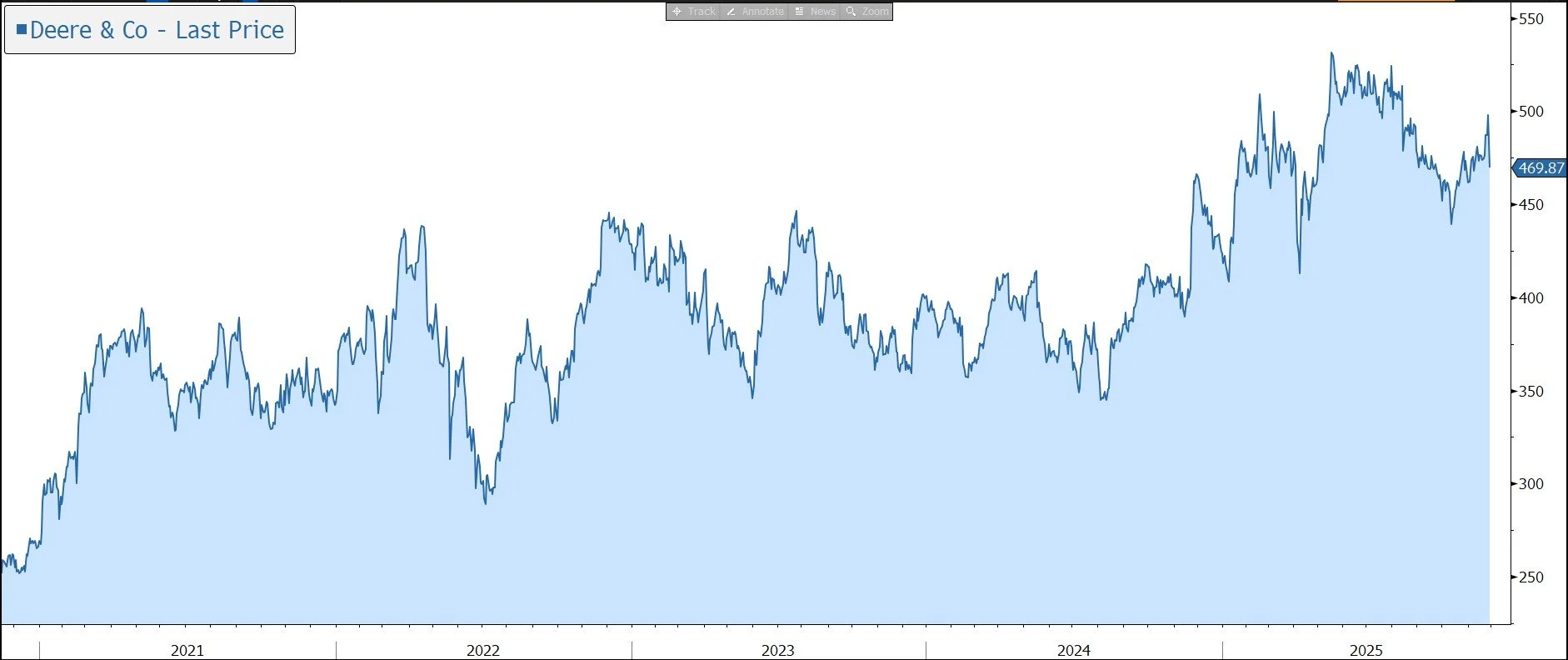

Earlier in the week, Deere & Company released results for the financial year to 2 November 2025. Despite ongoing market challenges, the numbers were slightly better than expected due to a robust finish to the year. However, the guidance for the new financial year was weaker than forecast as margin pressure from tariffs will continue to weigh on its large farm equipment unit. In response, the shares were marked down by 6% in US trading hours.

Deere is a global agricultural and construction equipment company with annual sales of almost $46bn. The group has a strong track record of innovation, a comprehensive distribution infrastructure, and global after-market capability. The group’s strategic aim is to outpace industry growth and generate a mid-cycle operating margin of 15%.

The business is benefitting from broad trends based on population and income growth, especially in developing nations, which are driving agricultural output and infrastructure investment. In addition, technological advances and agricultural mechanisation are expanding existing markets and opening new ones by helping customers increase their productivity, profitability, and sustainability.

The company believes it has incremental addressable market opportunities of more than $150bn that can be targeted through engaging with more customers and increasing levels of connectivity. The focus is on helping customers manage higher costs and increasingly scarce inputs, while improving their yields, using Deere’s integrated technologies.

However, in the near term, conditions in the global agricultural and construction sectors have been challenging because of higher interest rates, squeezed farming incomes, and lower government support. More farmers have switched to renting tractors and other equipment, and Deere has been forced to streamline field inventory.

During the latest financial year, worldwide net sales and revenue fell by 12% to $45.7bn, while net sales of equipment declined by 13% to $38.9bn. In the final quarter, worldwide net sales and revenue rose by 11% to $12.4bn, while net sales of equipment were up 14% to $10.6bn, ahead of the market forecast of $9.85bn.

Net income fell by 29% in the year to $5.03bn, in the middle of the guidance range of $4.75bn-$5.25bn, which has been lowered during the year. Profits were held back in part due to higher tariffs. In the final quarter, net income declined by 14% to $1,065m, while EPS also fell 14% to $3.93, slightly above the market forecast of $3.85.

The Production & Precision Agriculture segment includes large and certain mid-size tractors, combines, cotton pickers, sugarcane harvesters and loaders, and soil preparation, seeding, application and crop care equipment. Full-year sales declined by 17% to $17.3bn, in the middle of the 15%-20% guidance range. During the final quarter, sales rose by 10% to $4.74bn due to higher shipment volumes and favourable price realisation. Operating profit declined by 8% to $604m, due to higher production costs and higher tariffs, partially offset by price realisation and higher shipment mix. The margin slumped from 15.3% to 12.7%.

The Small Agriculture and Turf segment includes certain mid-size and small tractors, as well as hay and forage equipment, riding and commercial lawn equipment, golf course equipment, and utility vehicles. Full-year sales declined by 7% to $11.2bn, slightly better than the guidance for a 10% decline. During the final quarter, sales rose by 7% to $2,457m, due to higher shipment volumes. Operating profit was down 89% to $25m, due to higher tariffs, warranty expenses, and production costs. The margin fell from 10.1% to 1.0%.

Construction & Forestry full-year sales declined by 12% to $11.4bn, in the middle of the 10%-25% guidance range. In the final quarter, sales grew by 27% to $3,382m, while operating profit rose 6% to $348m primarily due to higher shipment mix, partially offset by increased production costs driven by higher tariffs.

The group’s Financial Services division reported adjusted net income grew by 25% to $1,114m. In the final quarter, it rose 69% to $293m, due to favourable financing spreads, some special items, and a lower provision for credit losses.

Deere’s balance sheet is fairly robust, with net debt of $54bn, a level consistent with supporting a credit rating that provides access to low cost and readily available funding. The group has a policy to raise its dividend “consistently and moderately”, targeting a 25%-35% payout ratio of mid-cycle earnings. The latest annual dividend was raised by 10% to $6.48 per share.

Looking forward, the company believes 2026 will mark the bottom of the large agricultural equipment cycle. While ongoing margin pressures from tariffs and persistent challenges in the sector remain, the group’s commitment to inventory management and cost control, coupled with expected growth in small agriculture & turf and construction & forestry, positions the company to effectively manage the business. Against this backdrop, net earnings are forecast to fall again from $5.0bn to $4.0bn-$4.75bn, slightly below market expectations. Operating cash flow of $4.0bn-$5.0bn is forecast. By division, net sales are expected to decline by 5%-10% in Production & Precision Agriculture and be 10% higher in both Small Agriculture & Turf and Construction & Forestry.

Source: Bloomberg